🦄 Dilution & Terms: What to Expect Going from Seed to Series-B and Beyond

🦄 Dilution & Terms: What to Expect Going from Seed to Series-B and Beyond

Let's address a common question amongst founders: what level of dilution is acceptable and how you should raise your early rounds

Welcome to the 44 new Fundraisedd people who have joined us since last Monday. If you’re reading this but haven’t subscribed yet, join the Fundraisedd community now by clicking this here button:

Hello friends,

Welcome to Fundraisedd, the newsletter that tells you all you need to know about fundraising and startup finance.

Hello to all the new subscribers who’ve joined this week, the community is going on 450 members! Your support means a lot to me 🥳

This week, we’ll address the topic of dilution and fundraising round structure, from Angel/Seed up to Series-B.

🌱 Angel / Seed

💧 Expected dilution? 10-15%

⌚ How long to raise? A few weeks up to a few months.

🏃🏽 Runway? 12-18 months

💵 Who invests? FFFs, HNWIS, or Seed funds

📆 When? Early in the life of a company, from 0 to a few 00’000s ARR

📜 Paperwork? Keep the contracts as simple as possible (KISS). This includes the investment contract and the Shareholder Agreement.

📜 Paperwork? At this stage, consider Convertible Notes and SAFEs.

🔎 Due Diligence? Basic, business model, financials, team

🎯 Founders’ objective? Find suitable investors who will believe in you, your team, and your vision.

🎯 Founders’ objective? Don’t get into complex contract structures.

💺 Board of Directors? People who invest will often ask for a Board Seat. If they are what is called “smart money,” this could prove highly beneficial to you.

💺 Board of Directors? If it’s only to control their investment, you may end up with a dysfunctional board. ⚠️

🌿 Series-A

💧 Expected dilution? 20-30%

⌚ How long to raise? 3-6 months.

🏃🏽 Runway? 18-36 months

💵 Who invests? VC funds, your previous investors, HNWIs

📆 When? Product-market fit has been found, 1M+ ARR (or on track to), growth phase

📜 Paperwork? Contracts get more complicated, more warranties & representations, more control given to the Board.

📜 Paperwork? Probably done through a Capital Increase (straight equity) but can also be a convertible note.

🔎 Due Diligence? Deeper, business model, financials, tech, HR

🤼 Team Compensation? If no ESOP has been implemented from the start, investors will ask for one to incentivise managers and key employees (long-run ESOP target size: ~20%)

🎯 Founders’ objective? Find investors who are willing to take you to the next step (B, C,…) and, eventually, to the end.

🎯 Founders’ objective? Find investors who will be ready to follow-on and support through your next financing rounds.

💺 Board of Directors? At this stage, you will have to give up Board Seats. However, don’t see it as a negative.

💺 Board of Directors? When smart, professional investors come in, their presence at the Board table will help your company tremendously.

🌳 Series-B and beyond

💧 Expected dilution? 20-30% per round (less if you achieve amazing growth and can command a high valuation)

⌚ How long to raise? 3-9 months.

🏃🏽 Runway? 24-36 months

💵 Who invests? VC funds, PE funds, Banks, Large corporations

📆 When? Expanding internationally, on track to go from a few M+ ARR to 10M+ ARR in 2 years (if you follow the T2D3 model)

📜Paperwork? Contracts get more complicated. Probably done through a Capital Increase, may include warrants, options, anti-dilution clauses,…

🔎 Due Diligence? Full-on. Business model, financials, tech, HR, legal, health & safety, policy, regulation, corporate governance,…

🤼 Team Compensation? ESOP will be topped up to plan for large expansion of workforce.

🎯 Founders’ objective? Investors are coming in to set you (and them) up on the path for a profitable exit or IPO. Find people who will help you reach these goals.

💺 Board of Directors? Going forward, your Board will look totally different.

💺 Board of Directors? There will be a strong expectation of professional corporate governance which means more non-executive board members and more oversight.

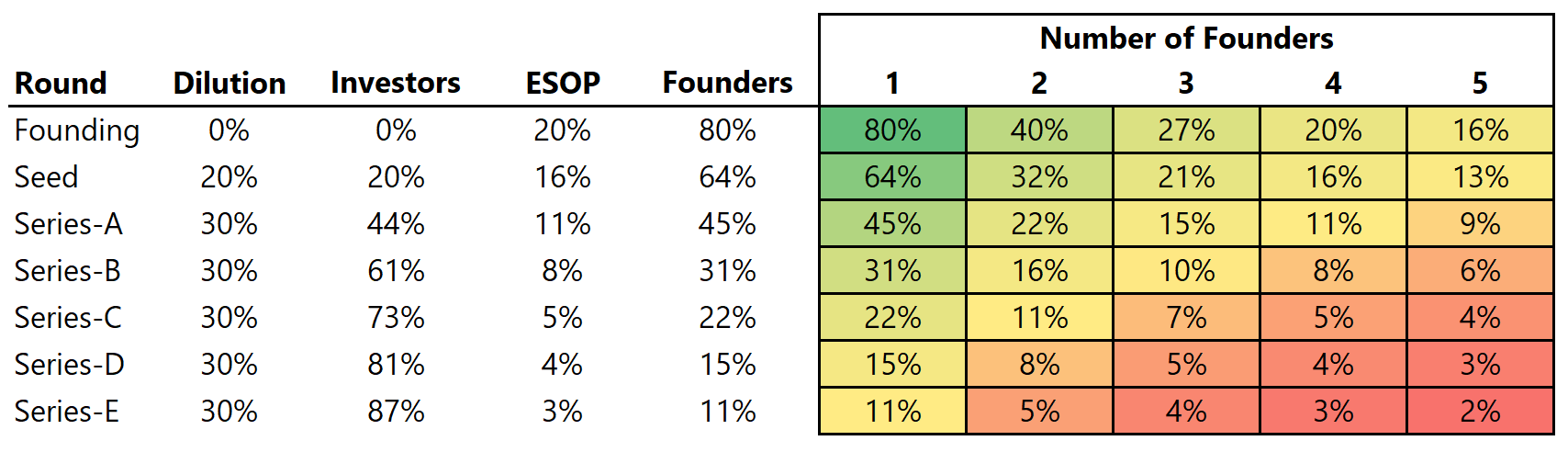

Summarising the dilutive effect of a series of fundraising round in an Excel table gives you an idea of where you’ll end up as a founder/co-founder (this is an exercise I invite you to do!):

This article and infographics by Mark Suster is also a great resource on the topic of dilution.

This Twitter thread, which I already shared, is also an important warning about early-stage dilution. Don’t be over enthusiastic with converts and lose track of your total dilution!

On the topic of employee share compensation, this amazing data analysis by Leo Polovets of salaries and equity grants based on AngelList data.

Drop your comments on the article and let’s discuss the topic of dilution and ownership this week!

Have a great Monday and rest of the week,

Best,

Nicolas

I love this article because I am a first time entrepreneur trying to answer questions such as How much should we target for dilution pre series A? What sort due diligence is reasonable etc... This is a great cheat sheet! Thank you!